Are Interest Rates a Scapegoat for Value’s Rocky Road?

Anyone paying attention to the markets over the past several years is well aware of the tough times Value investors have faced, especially compared to their Growth-focused counterparts. Some have argued that Value’s downfall has been driven by the new normal of low interest rates and flattening / inversions of the yield curve. However, recent research by AQR debunks this theory and shows that interest rates have had little explanatory impact on the troubled returns for Value and that they will have little to do with a potential rebound in the future.

We decided to further extend AQR’s analysis by leveraging multi-factor risk models to provide a ‘pure’ perspective on Value and interest rates. Since a discussion about Value is often complemented by a discussion on Growth, we also extend the analysis to look at impact of interest rates on Value vs. Growth from a factor perspective.

Factor Mimicking Portfolios: A “Pure” Look at Value and Growth

To create a pure view on Value and Growth, we leveraged factor mimicking portfolios from Axioma’s US 4 Medium Horizon risk model, with history from May 2017 to present. The idea behind a factor mimicking portfolio (FMP) is to use an optimizer to create a market-neutral portfolio that has an exposure of 1 to a given factor and an exposure of 0 to all other factors in the model. FMPs represent the performance of the respective risk model factors and allow us to see the security and exposure characteristics of the factors. In this case, we’ve created FMPs for Value and Growth.

Are Interest Rates a Character in the Value vs Growth Story?

Sticking with the approach of using pure factor models for our analysis, we chose to introduce impact from interest rates by leveraging a regression-based interest rate factor from a macroeconomic risk model. Axioma offers a US macroeconomic risk model which includes an interest rate factor; however, we chose to use Wolfe Research’s QES US Broad risk model to have a more ‘unbiased opinion’ in the analysis.

Wolfe Research defines their Interest Rate Beta factor as the beta to interest rate changes for US Treasuries approximately equivalent to the 10Y. To get a sense of the typical Interest Rate Beta sensitivity across portfolios, we can look to Wolfe’s risk model factsheet, where they show the exposures of all factors across US portfolios proxied with 13F holdings data. The mean Interest Rate Beta exposure is around 0 but ranges from a little over +2 to -2.

Looking at our Value FMP against the Wolfe risk model since 2017 using the chart below, we can see that, as expected, there’s a high positive exposure to the Book-to-Price factor and a negative exposure to the Growth factor. Interestingly enough, the Growth factor exposure turns positive after March 16, 2020, coinciding with the recent market downturn. The real focal point here, however, is the Interest Rate Beta factor, which has a relatively neutral exposure around 0.1 for the majority of the period. While an average exposure of 0.1 is higher than the mean exposure of US portfolios, it’s still well within the middle 50% of the distribution, as shown in Figure 3. Although the exposure jumps slightly to around 0.28 by the end of the period, overall we can deduce that the Value FMP does not have an unusually high exposure to the Interest Rate Beta factor.

We can also review the Value FMP factor exposures relative to the Growth FMP. The trend is largely similar on an active basis, with Book-to-Price showing high positive active exposure, Growth showing low negative active exposure, and Interest Rate Beta showing moderate active exposure. The active Interest Rate Beta exposure is higher than the absolute exposure, indicating that the Value FMP is more exposed to interest rate changes than the Growth FMP, though based on the magnitude of the active exposure, Growth does not have an unusually low exposure to Interest Rate Beta.

Turning to performance, the Value FMP underperformed the Growth FMP by -11.8% for the May 2017 to July 2017 period. Decomposing this active performance by factors shows an interesting, but unsurprising trend based on our exposures analysis. Here, we see that the Book-to-Price factor explains almost half of the underperformance, with -5.73% drag from this factor. Leverage is the next highest performance detractor, with -1.87% drag. Finally, in third place, comes Interest Rate Beta, with -1.15% performance drag.

Even though Interest Rate Beta does show up as the third highest factor contributor, it explains less than 10% (= -1.15% / -11.8%) of the overall underperformance of Value vs Growth. We also ran factor attribution on an absolute basis for only the Value FMP, and Interest Rate Beta was an even smaller contributor to performance, explaining about 5% of the overall negative performance. From a pure factor lens, it seems that Interest Rate Beta does not have meaningful explanatory power for Value’s tough performance, both on an absolute basis and relative to Growth. Rather, the best way to explain Value’s lackluster performance is... Value just being Value.

We chose to focus the analysis here on Wolfe’s Interest Rate Beta factor to gain an unbiased opinion on the Value and Growth FMPs, but we also ran the same analysis after-the-fact with Axioma’s macroeconomic model. The conclusions were largely the same, with Axioma’s interest rate factor explaining a lower portion of the returns as compared to Wolfe’s interest rate factor. This gives us even less reason to believe that the interest rate environment is the driver of returns for Value portfolios.

This analysis should actually provide some comfort for Value investors. It seems unlikely that rates will be rising anytime soon given that the US is in the throes of pandemic-induced recession; however, perhaps this is no matter to Value and despite the rocky road traversed over the past decade, there may be clearer paths up ahead for Value investing that are independent of the interest rate environment.

US & Global Market Summary

US Market: 7/27/20 - 7/31/20

- The US market powered through the worst GDP print in the country’s history to end up on the week, sparked by some massive tech earnings beats.

- Annualized GDP fell 32.9% from April to June, driven by the contraction in consumer spending, as well as weak exports, inventories, business and residential investment, and state and municipal government spending. This was slightly better than the -34.5% consensus forecast.

- The neutered outlook for an economic recovery precipitated a rally in Treasuries, leading to 10-year Treasury yields falling to near record lows.

- 1.434 million Americans filed for state unemployment benefits last week according to the BLS, the second consecutive rise in weekly jobless claims since the jobs market cratered in March.

- Big tech continues to fuel the market, as Amazon, Apple, Google, and Facebook all beat (or shattered, in some cases) consensus estimates.

Normalized Factor Returns: Axioma US Equity Risk Model (AXUS4-MH)

- Momentum was the week’s biggest winner as it climbed +0.16 standard deviations higher into Overbought territory.

- Market Sensitivity saw a slight uptick as it remains Oversold at -1.26 SD below the mean.

- Size appears to have peaked at +1.15 SD above the mean on 7/24, and has already reverted enough to lose its Overbought status.

- Volatility continued to see weakness on a normalized basis, falling by -0.26 SD (compared to -0.43 last week), and earning an Extremely Oversold designation.

- US Total Risk (using the Russell 3000 as proxy) declined at a faster pace relative to last week.

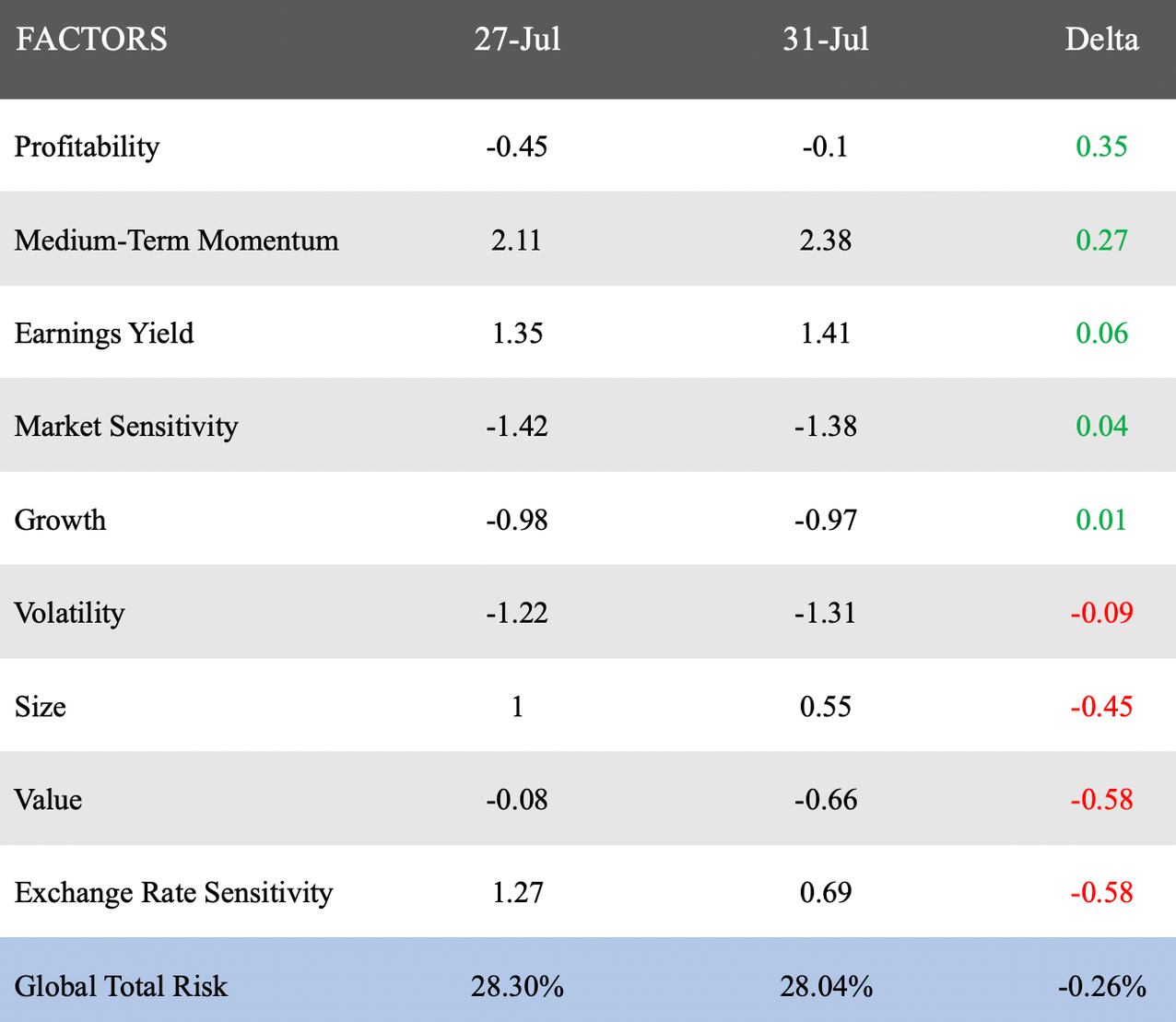

Normalized Factor Returns: Axioma Worldwide Equity Risk Model (AXWW4-MH)

- Profitability was again the top performer globally, and has climbed out of negative space to become almost perfectly neutral.

- Strength in Momentum continued as it moved higher into Extremely Overbought space at +2.38 SD above the mean.

- The decline in Size appears to have accelerated, as it exited Overbought space and fell 0.45 SD towards the mean.

- Value saw significant weakness as it fell deeper into negative territory by -0.58 standard deviations.

- Exchange Rate Sensitivity also declined by -0.58 SD, and has shed its Overbought designation. Recall that this factor peaked at +2.62 SD above the mean on 7/9.

- Global Risk (using the ACWI as proxy) declined by 26bps.

Regards,

Alyx