Factor or Alpha Driven? Interpreting The Recent Market Environment

We hope you had a relaxing holiday season and would like to wish you and your families a happy, healthy, and successful 2023!

The first week of January is often a good time to reflect on the prior year. Many of our readers are actively working on their 2022 communication to their stakeholders, summarizing key strategy metrics, lessons learned, and potential improvements for the future.

To help put 2022 in context, we’re kicking off our 2023 Factor Spotlight series leveraging Omega Point’s quantitative lens to help interpret the recent market environment. Throughout 2022, equity markets presented investors with a myriad of challenges, particularly those investors who are fundamentally-driven stock-pickers. Many have felt the factor-driven nature of stock prices governed by persistent post-COVID supply chain issues exacerbating inflation, a hawkish FED, and recession fears, all on top of geopolitical turmoil. To put the prior year into perspective, we set out to answer the question: “Contextually, how significant was the role of factor volatility in the recent market downturn?

In May 2022, we introduced the Extreme Movers Portfolios to quantify how “factor-driven” or “alpha-driven” the equity markets are weekly. With 2022 behind us, we expanded the Extreme Movers framework historically to provide context for the recent market period and provide a standardized framework with which to categorize future market regimes.

In summary, we found:

- 2022 was the most factor-driven / least alpha-driven year since Jan 1, 2007, the start date of our analysis.

- Weekly market volatility in 2022 reached the highest levels since the 2008 Global Financial Crisis.

- 2022 surpassed every year historically in combined market volatility and factor influence.

2007 - Present: Classifying “Factor-Driven” and “Alpha-Driven” Markets

This week, we’ll focus on the US market using our US Extreme Movers Portfolio. The portfolio is a weekly-rebalanced, market-neutral portfolio that invests long in the top decile of best performers and shorts the bottom decile of performers in the Russell 1000 index. The portfolio’s characteristics and performance point to the areas of the market that were in and out of favor and provides valuable insight into what, thematically, directed stock returns.

Our US Extreme Movers portfolio began on Jan 1, 2007. Each week, we observe performance decomposition through the lens of various risk models to identify quintiles that best categorize the spectrum of the most “Alpha-Driven” weeks to the most “Factor-Driven” weeks.

To calibrate our classification, we took the total sample of all weeks (>800) since Jan 1, 2007, and ranked them by Alpha Contribution to return percentage.

A Very Alpha-Driven Week (Top Quintile) is one where an Alpha Contribution to return is HIGH and a Very factor-driven Week (Bottom Quintile) is one where Alpha Contribution to return is LOW.

Below are the Alpha Contribution thresholds that demarcate the quintiles:

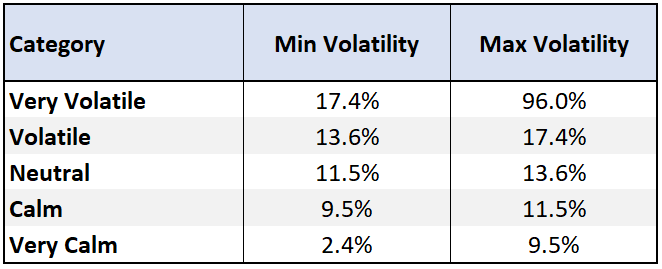

In addition to understanding what portion of the market volatility was attributable to factors and alpha, we also need to proxy the market volatility levels. We applied the same ranking methodology to categorize the volatility of weekly periods based on the total return of the US Extreme Movers portfolio.

We categorized these quintiles from “Very Volatile” to “Very Calm.”

To break down the historical context, we segmented the historical data by calendar year and market regime to give investors a sense of how the recent and current market stack up against prior periods. In addition, we’ve included details on the thematic market regimes below.

Aggregating Weeks into “Alpha-Driven” vs. “Factor-Driven” Periods

For fundamental investors, alpha availability is critical. Historically, there have been periods during which the majority of volatility in the market was attributable to stock-specific nuances. These periods provide a fertile ground for stock-pickers’ competitive advantage to thrive. However, other periods were clouded by market factors restricting investors’ ability to drive idiosyncratic returns.

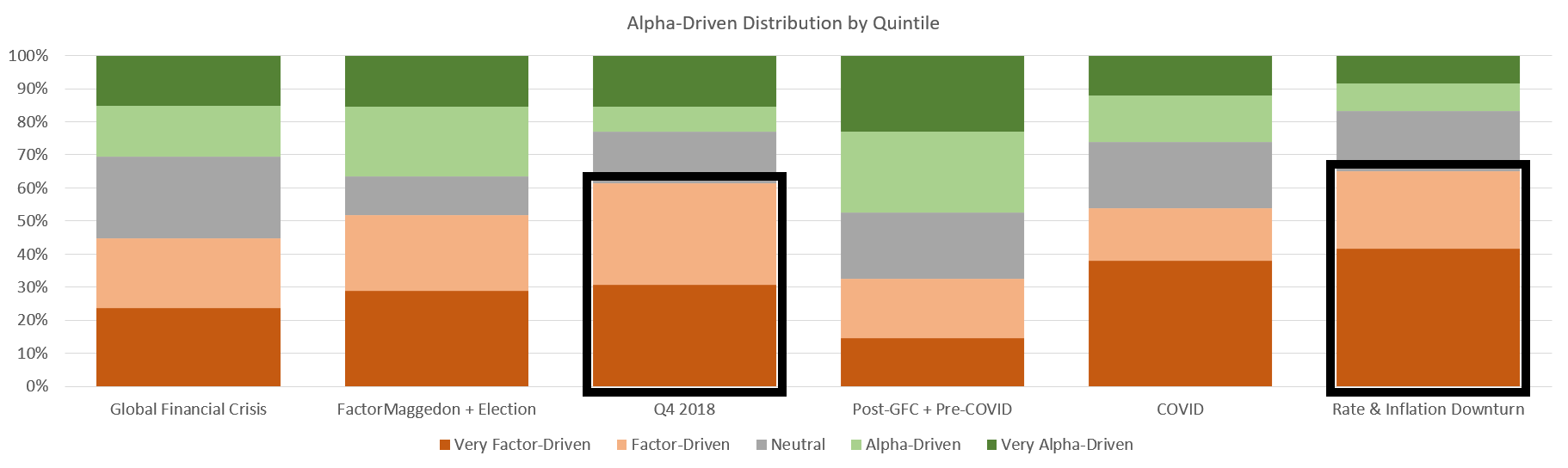

Below, we broke down the percentage of weeks each year since 2007 on a scale from “Very Factor-Driven” to “Very Alpha-Driven.” In doing so, we found that 67% of the weeks in 2022 were at least “Factor-Driven,” which is the highest percentage observed since the beginning of 2007. Conversely, only 16% were at least “Alpha-Driven,” which means that bottoms-up, fundamental stock-pickers were fighting an uphill battle to uncover opportunistic stocks whose prices weren’t over-influenced by market and macroeconomic forces.

When segmenting by market regime, the “Rate & Inflation Downturn” period, which we define as starting in November of 2021 on supply chain constraints and increased inflation fears, showed the smallest percentage of “Alpha-Driven” weeks and the most “Factor-Driven” weeks. Interestingly, even the Global Financial Crisis period presented significantly more alpha opportunity and less factor influence than the most recent period. Q4 2018 was the most similar period though we know that the most recent environment has been much more persistent.

Aggregating Weeks Into Volatile vs. Calm Periods

The breakdown of Extreme Mover's performance into factor and alpha is only part of the story. The recent US market regime has not only been dominated by factors but has been historically volatile. Below, we aggregated each week, classified from "Very Calm" to "Very Volatile," across calendar years and market regimes. We found that 82% of weeks in 2022 were either "Volatile" or "Very Volatile," which marks the highest percentage recorded since 2008.

Following the Global Financial Crisis, we saw ten years of low volatility in the US. Except for Q4 2018, more than half of the weeks from January 2010 to December 2019 were "Calm" or "Very Calm." Volatility levels during the subsequent COVID regime and the Rate & Inflation Downturn regime were highly similar and represented the highest levels since the Global Financial Crisis.

Elevated Volatility with Factor Influence: The Perfect Storm

We've seen that the recent environment has been historically factor-driven and historically volatile. To round out our analysis, we wanted to identify the cross-section of the two. In other words, "how often was the US market heavily volatile because of factors?" This intersection is critical to define because it presents a challenging environment for fundamental investors. During these periods, alpha is far less available, but stock prices are experiencing significant price movements.

The chart below presents the percentage of weeks each year categorized as at least "Factor-Driven" and "Volatile." When framed in this context, 2022 surpasses every other year historically as 59% of weeks in 2022 were both high in volatility and factor influence, and 25% of weeks were "Very Factor-Driven" and "Very Volatile" (meaning they were in the top quintile of historical periods in both categories).

COVID and the Rate & Inflation Downturn periods outpaced the GFC in terms of factor-driven risky weeks. Those two recent regimes account for 26 months of the last three years.

Leveraging Our Framework to Measure Future Market Conditions

Now that we have a framework in place for quantifying and categorizing periods by volatility and alpha vs. factor influence, we have the ability to help investors quickly recognize when markets might be rich with alpha or, just as importantly when factor volatility is the dominant force. In our future editions of factor Spotlight, we will highlight what we see across the equity landscape and how investors can take action to protect against factor headwinds and maximize alpha.

If you have any questions or want to discuss our Extreme Movers analysis in greater detail, don't hesitate to reach out!

Regards,

Kevin