The Factor Signature of Volatility

Volatility continues spiraling downwards as the factor seemingly marches back to the beat of its old drum. As we highlighted in last week’s Factor Spotlight, Volatility spent almost the whole of 2020 skyrocketing with positive performance; however, performance since February 2021 would show that the factor may be coming back down to earth.

Volatility’s performance over the past month was particularly hard hit, with the factor showing the worst performance of all style factors in the Axioma US 4 Medium Horizon (“Axioma US4”) risk model.

Last week, we focused on the performance behavior of high and low volatility stocks. We showed evidence that low volatility investing may be re-emerging as investors start to favor low volatility and shy away from high volatility as the economic reopening continues.

This week, we review the factor characteristics of high and low volatility stocks to understand the forces at play better.

Volatility’s Crowding and Macro Factor Exposure

We’ll continue to work with the High Volatility and Low Volatility portfolios from last week for our analysis. Though we constructed these portfolios using the Axioma US4 risk model, we can leverage the multi-model framework of the Omega Point platform to evaluate these portfolios through the lens of the Wolfe QES US Broad (“Wolfe US Broad”) risk model. In particular, this model will help us better to understand the crowding and macro characteristics of volatility.

The three factors of focus from the Wolfe US Broad model are the Hedge Fund Crowding (“HF Crowding”), Short Interest, and Interest Rate Beta factors:

HF Crowding

A look at the exposure of the HF Crowding factor on the High and Low Volatility portfolios helps us understand if institutional investors are piling into these themes.

The chart below shows us the HF Crowding exposure for our portfolios since January 2020.

Though the HF Crowding exposure for the Low Volatility portfolio was positive for much of 2020, we see that after a peak in April 2020, right after the initial COVID de-leveraging, the exposure starts to trend downward steadily. The decreasing exposure shows us that low volatility themes were trending out of favor for long investors throughout this time. However, despite a sharp downturn in February, March, and April of 2021, a strong rebound emerged since May, signaling that investors are heading back to low volatility stocks.

Much of the intersection between low volatility and crowding can be captured in the sector exposures. As rates have stabilized in the past several weeks, investors are beginning to favor defensive growth & technology names. This move back towards defensive technology stocks has allowed them to re-emerge as steady-eddy, low volatility names, which we see reflected in the skyrocketing technology sector exposures of the Low Volatility portfolio.

This move back towards defensive technology stocks has allowed them to re-emerge as steady-eddy, low volatility names, which we see reflected in the skyrocketing technology sector exposures of the Low Volatility portfolio.

While the High Volatility portfolio was biased away from long crowding before the COVID era (and is generally anti-long crowding), that trend intensified after Vaccine Monday in Nov 2020 and has generally been trending downward since then. June and July 2021 show hints of a slight rebound in the HF Crowding exposure for high volatility stocks, but overall, investors are still shying away from this segment.

Short Interest

Turning to the Short Interest factor allows us to see a similar view on crowding for institutional short books.

The story around short crowding is more centered around the high volatility theme than the low volatility theme, as one might expect. Pre-COVID, we see a positive exposure to the Short Interest factor for the High Volatility portfolio. As the economic fiscal stimulus kicked in and Volatility oddly started to be favored by the market, investors backed off from betting against high volatility - this is evident by the declining exposure of the High Volatility portfolio throughout most of 2020 and early 2021. June and July 2021 show an increase in the short crowding exposure as investors’ nerves around high volatility begin to wane and confidence in betting against volatility strengthens.

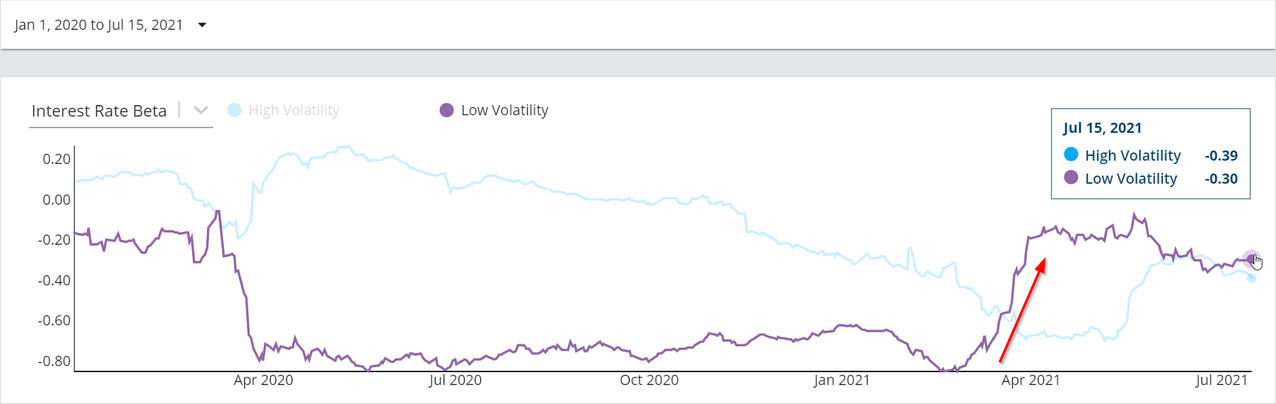

Interest Rate Beta

A macro lens illustrates that volatility investing is influenced by the interest rate environment, particularly for low volatility.

As the March 2020 downturn hit the market and rates seemed destined to stay low for the foreseeable future, the Interest Rate Beta exposure for the Low Volatility portfolio plunged and remained at all time (since 2007) lows for the rest of 2020 and into 2021. However, once rates began to rise, the Interest Rate Beta exposure popped up as well, with a sharp upturn in March and April 2021.

It’s possible that the trend we see here is connected to the defensive nature of stocks that are typically low volatility. Low volatility is normally associated with higher dividend payers and defensive securities, which are favored in a low rate environment. As rates go up, these names become less favorable and are likely to be sold off, which increases their volatility and moves them out of the Low Volatility portfolio.

In the chart above, we see this exact trend play out, with the Low Volatility portfolio showing a positive Dividend Yield exposure throughout 2020 when rates are stable and low. As expectations of rates rising hits the market February and March 2021, the Dividend Yield exposure drops, indicating that the high dividend payers have moved out of the Low Volatility portfolio.

As rates have stabilized over the past several weeks, we’ve seen signs of a slight lift in the Dividend Yield exposure. As we noted with the recent sharp increase in the technology sector exposure for the Low Volatility portfolio, the trends in low volatility can be closely linked with investors’ outlook on defensive dividend payers and the rate-driven environment.

Volatility Has Never Been Riskier

Perhaps the most unsettling (or exciting - depending on your risk tolerance) aspect of Volatility’s re-normalization is the uncertainty of the factor, as quantified by factor volatility. Factor volatility tells us how much we expect the factor to move in the future and the Axioma US 4 risk model provides a predicted estimate around this measure.

The chart above accentuates the precarious nature of Volatility in the current environment, as this factor’s uncertainty reaches new heights relative to the history since 2007.

To put context around this, we can interpret this to mean that if the current predicted volatility of 10.7% is realized, we would expect the factor to move 10.7% on an annualized basis, or ~3% monthly. Thus, all else equal, it would only take an absolute exposure of 0.16 to move the portfolio by 50 bps within one month (50 bps / 3% = 0.16).

Below is a list of the top ETFs by average daily trading volume and their respective Volatility exposures.

6 of the top 15 ETFs have exposures > the 0.16 threshold, and an additional 3 have exposures that are very close to the threshold. Suppose these widely used ETFs have exposures at these levels. In that case, we can imagine that the portfolios of fundamental investors are likely also susceptible to Volatility exposure that can rock their performance if the Volatility re-normalization continues.

In the coming weeks, we’ll continue to help investors understand the behavior of the notorious Volatility factor and present solutions on how to neutralize its contribution to portfolio risk.

US & Global Market Summary

US Market: 07/12/21 - 07/16/21

- The US market slid over the course of the week as inflation concerns continued to weigh on investors’ minds, despite strong retail sales data and better-than-expected earnings reports from some major banks.

- The major US indices reversed course after hitting record highs over the past few weeks, with the S&P 500 down 1% and Nasdaq down 1.8%.

- The Consumer Price Index climbed at a pace not seen since August 2008, up 5.4% YoY vs. a consensus forecast of 4.9%. Core inflation came in at 4.5%, the largest increase since 1991.

- Yield on 10-year US Treasuries dropped to 1.3%, as the bond market didn’t seem to react to inflation fears as much as equities.

- On Wednesday, Fed Chairman Powell said that the economy is “a ways off” from a point where the central bank would change its current accommodative policy. He attributed the notable increase in inflation to temporary factors.

- Democrats on the US Senate Budget Committee reached an agreement on a $3.5T human infrastructure investment, which may be part of the budget resolution to be debated later this summer. A $600B bipartisan infrastructure package is also in the works.

Normalized Factor Returns: Axioma US Equity Risk Model (AXUS4-MH)

- Profitability again topped the leaderboard as it crossed over the historical mean into positive normalized territory.

- Earnings Yield saw another week of strength, moving up nearly half a standard deviation as it continued to recover from its 6/24 trough of -1.86 SD below the mean.

- Value saw just enough positive movement to exit Extremely Oversold space, now sitting at -1.92 SD below the mean.

- Growth rose by +0.16 standard deviations and is close to becoming an Extremely Overbought factor at +1.89 SD above the mean.

- Market Sensitivity fell sharply out of Overbought space, tumbling by 0.61 standard deviations away from recent peak of +1.7 SD above the mean on 7/1.

- As discussed earlier, Volatility was the worst performing factor for the second straight week as it dropped out of Overbought space after falling 0.65 standard deviations to +0.99 SD above the mean.

- US Total Risk (using the Russell 3000 as proxy) decreased by 38 basis points.

Normalized Factor Returns: Axioma Worldwide Equity Risk Model (AXWW4-MH)

- Profitability was also the week’s biggest winner worldwide as it rallied by +0.57 standard deviations towards the mean. It remains an Oversold factor at -1.41 SD below the mean.

- Earnings Yield continued along a positive path as it climbed higher away from the mean.

- Global Growth garnered an Overbought designation as it moved up to +1.1 SD above the mean.

- Value continued its descent further into Extremely Oversold territory, albeit at a slower clip than last week’s decline.

- Global Volatility also saw another precipitous drop, falling out of Overbought space with a -0.71 standard deviation move, landing at +0.63 SD above the mean.

- Global Total Risk (using the ACWI as proxy) decreased by 36 basis points.

Regards,

Alyx