With Rising Rates Comes A Rebound in Value

The past few weeks have had investors scratching their heads as we’ve seen rates surging in 2021. Long-term US treasury yields have risen over 50 bps since the end of 2020, with the majority of that rise happening in the past month alone. Coupled with the January retail crowding event and the recent market sell offs that have posed unusual challenges for the typically-soaring tech stocks, investors are likely wondering what might be causing this tumult.

Many are noting that the economic re-opening trade that has been looming since we got an initial taste in November 2020 on the Pfizer vaccine news might finally be here, which is causing interest rates to run haywire. As Bloomberg notes, “traders are moving in sync on the belief that the most ambitious vaccination campaign in history is about to supercharge economic growth and unleash price pressures that have long been dormant”.

To provide insight into this belief, we will leverage our trusty risk model magnifying glass to evaluate the drivers of the recent market shifts as they relate to sensitivity to interest rates.

Revisiting the Value Story

Last summer, we ran an analysis to understand how much the extended low interest rate environment influenced the underperformance in value relative to growth strategies that has prevailed for the past several years. In order to define “pure” Value and Growth portfolios, we used factor mimicking portfolios (FMP) from the Axioma US 4 Medium-Horizon (“Axioma US 4”) risk model that leverage optimization to create a portfolio which has an exposure of 1 to the target factor (i.e. Value or Growth) and an exposure of 0 to all other factors.

We then used the Wolfe Research QES US Broad (“Wolfe US Broad”) risk model, which includes an Interest Rate Beta factor, to understand the impact of interest rate sensitivity on the active performance of the Value FMP vs the Growth FMP. We concluded that though Value had a decent overexposure to the Interest Rate Beta factor, this factor did not explain much of the active performance between the two FMPs. For more details on our methodology and analysis, please see our prior Factor Spotlight post, Are Interest Rates A Scapegoat for Value’s Rocky Road.

We are revisiting this analysis to see if there had been any change in the influence of interest rate sensitivity on the Value vs. Growth FMP performance. Before we dive into the update, recall that the Wolfe US Broad risk model defines Interest Rate Beta as the beta to interest rate changes for US Treasuries approximately equivalent to the 10Y. This means that a portfolio with positive exposure should outperform (underperform) on rising (falling) rates, and a portfolio with negative exposure should outperform (underperform) on falling (rising) rates.

Not much has changed in terms of factor exposures from our prior analysis, with the Value FMP continuing to be overexposed to the Interest Rate Beta factor relative to Growth FMP.

However, in a major shift from our prior analysis, the Value FMP relative to the Growth FMP shows an active performance of 2.2% on a YTD basis. This tells us that the long-term Value vs Growth trend is likely reverting, with Value now outperforming Growth. Conversely to what we observed in our prior analysis, a decomposition shows that the Interest Rate Beta factor explains almost 60% (= 1.3% / 2.2%) of the active performance!

Given that Value is over-exposed to interest rate sensitivity relative to Growth, we would expect Value to outperform as interest rates are rising, which is exactly with the attribution tells us. While interest rates may not have had a big impact on the lull in Value investing over the past several years, they may be a part of the key to the Value resurgence as the economy continues on the path to recovery.

Is the Interest Rate Trade Crowded?

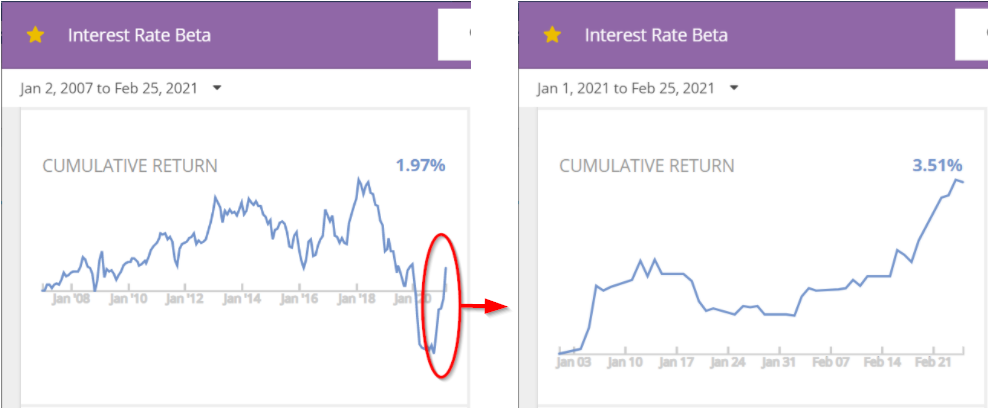

Along with the uptick in interest rates this year, we’ve also seen a massive rise in the performance of the Interest Rate Beta factor. On a YTD basis, the factor is up over 3.5%, which is one of the largest surges in this factor’s history.

Given this sharp behavior change, we zoomed in on the Interest Rate Beta factor to see if the characteristics of this factor could provide additional insight. To do this, we constructed a market-neutral high-minus-low (HML) portfolio based on this factor using the Russell 3000 universe. The long side of the portfolio is equal-weighted across all stocks with an Interest Rate Beta exposure greater than 1 and the short side is equal-weighted across all stocks with an Interest Rate Beta exposure less than -1.

One of the observations that emerged from reviewing the characteristics of the Interest Rate Beta HML is that the factor is exhibiting signs of crowdedness. The exposures for the HF Crowding and Short Interest factors, both of which measure stock crowding on both the long and short side, are at high points after a large hike in the exposures after “Vaccine Monday” in early November 2020.

Breaking the Interest Rate Beta portfolio into long vs short highlights that these trends are more heavily driven by the short side. In other words, the names that are underexposed to this factor (i.e. the names that are expected to underperform as rates rise) are becoming less crowded in both the long and short books of institutional investors.

While we haven’t yet seen investors piling into the names that have high sensitivity to interest rates, as is noted by the long side of the Interest Rate Beta HML showing little contribution to the change in the crowding exposures, it’s possible that we’ll start to see this reverse as the economy continues to open and rates continue to rise.

What Do the Correlations Say?

We’ll round out our analysis with a look at the correlations between Interest Rate Beta and Value as well as Interest Rate Beta and Growth, as estimated by the Wolfe US Broad risk model. While the correlations tend to fluctuate over time and even change signs from time to time, we observe that the correlations have reached extremes in 2020 and 2021.

Currently, the correlation between Value and interest rate sensitivity is at an all-time high, while the correlation for Growth is at an all-time low. This underscores the recent trend that we’ve been seeing and points to a continuation of the widening between the Value vs Growth spread as the economy re-opens and rates continue to rise.

Regardless of which side of the Value vs Growth argument you’re on, it’s clear that the re-opening trade may finally be upon us. If this is in fact the case, it may have lasting implications on the way Value and Growth behave going forward, as well as how investors re-position their portfolios to accommodate this shift in macro trends. If you’d like to discuss ways to evaluate the impact of interest rate sensitivity and the reopening trade on your portfolio, please reach out to us.

US & Global Market Summary

US Market: 02/22/21 - 02/26/21

- The market experienced a somewhat frenetic week punctuated by some wild swings across the board. Tech names were hit hard as the Nasdaq tumbled by 5%, its worst week since October 2020.

- As mentioned earlier, bond yields saw some atypically manic action as well, with 10 Year and 30 Year Treasuries notching their biggest monthly gains since 2016.

- “Stonks” were back on the menu as GME shot up 156%, reminiscent of that stock’s unprecedented action in January, and trading was halted on 15 penny stocks that had been targeted by social media users.

- Congress passed the $1.9T COVID relief bill on Saturday, mostly along party lines, setting the stage for a protracted battle over a minimum wage hike.

- On the earnings front, 95% of S&P 500 companies have now reported, tallying overall EPS growth of 4% (and beating consensus expectations).

Normalized Factor Returns: Axioma US Equity Risk Model (AXUS4-MH)

- As we discussed earlier, Value was the biggest winner, rallying into positive normalized space after a +0.48 standard deviation move.

- Market Sensitivity continued to rebound from Oversold territory after bottoming out at -1.23 SD below the mean on 2/4.

- Size continued its march back towards the mean, benefiting from a +0.35 standard deviation move after it exited Oversold space two weeks ago.

- Volatility took a tumble, falling nearly half a standard deviation and garnering an Oversold designation at -1 SD below the mean.

- Momentum fell by 0.56 standard deviations, shedding its Overbought label and now sitting at +0.69 SD above the mean.

- Growth saw a profound downward move, falling 0.82 standard deviations into negative normalized territory after peaking at+1.49 SD above the mean on 2/5.

- US Total Risk (using the Russell 3000 as proxy) decreased by 15bps.

Normalized Factor Returns: Axioma Worldwide Equity Risk Model (AXWW4-MH)

- Value topped the leaderboard again, moving up nearly half a standard deviation and landing in positive normalized space.

- Earnings Yield continued its climb back towards the mean after shedding its Oversold label two weeks ago.

- Exchange Rate Sensitivity has started to bounce back after nearly brushing Oversold territory at -0.94 SD below the mean on 2/22. It now sits at -0.86 SD below the mean.

- Momentum saw the week’s biggest move down, falling by 0.32 standard deviations and looking close to leaving Overbought space at +1.07 SD above the mean.

- Just as we saw in the US, Growth saw a huge downwards move, falling 0.83 standard deviations and simultaneously leaving Overbought space and approaching the mean.

- Global Risk (using the ACWI as proxy) declined only by 4bps.

Regards,

Alyx